Louie Valdez of Westlake Village, Former Financial Advisor

Millions of older adults and younger individuals with disabilities require assistance with daily activities that many take for granted.

According to LongTermCare.gov:

- About seven out of ten people turning 65 today can expect to need some form of long-term care services in their remaining years.

- Women need care longer (3.7 years) than men (2.2 years).

- Twenty percent will need long-term care for more than five years.

Confusion often surrounds the cost of long-term care and who is responsible for paying for it.

Louie Valdez of Westlake Village states, “According to a survey published late last year by KFF (entitled The Affordability for Long-Term Care and Support Services), a leading health policy organization in the U.S., nearly one in four adults mistakenly believe that Medicare will cover the cost of nursing home care for themselves or a loved one with a long-term illness or disability”.

Almost half, or 45%, of adults who are 65 years or older believe Medicare will pay these costs.

Let us be clear. Medicare and most health insurance, including Medicare Supplement Insurance (Medigap), do not pay for custodial care, such as helping with activities of daily living (ADLs), if that is the only care you need.

Medicaid pays for over 60% of long-term care residents, according to Louie Valdez of Westlake Village, CA.

Before we continue, let us define the two terms.

HHS.gov defines Medicaid as a “joint federal and state program that helps cover medical costs for some people with limited income and resources.”

Medicare is a “federal health insurance for people 65 or older, and some that are under 65 with certain disabilities or conditions.”

And here lies the problem that will affect many in retirement. Medicare is not responsible for covering long-term care costs. Medicare will only cover a limited stay in a nursing home following a qualifying hospitalization. Even then, out-of-pocket costs can add up.

Medicaid is the primary source of funds that pay for long-term care, but Medicaid places strict limits on income and assets, depending on the state and specific program. Moreover, Medicaid has a “look-back” period regarding your assets.

In most states, generally speaking, the look back is 60 months, per the American Council on Aging. California is 30 months, but that is expected to be completely phased out by July 2026. New York has no look back for Community Medicaid.

For most states, all financial transactions over the last 60 months are subject to review.

According to Louie Valdez of Westlake Village, CA, in practical terms, penalties could result if an audit finds a cash gift to your grandson for a high school trip, gifting property or cash to relatives, or selling assets below market value.

So, if Medicaid may not be an option for you, let us review some alternatives.

- Consider a health savings account (HSA). Those with high-deductible healthcare plans may be able to contribute to an HSA and withdraw funds to pay for eligible medical expenses. Contributions to an HSA reduce taxable income, appreciate tax-free, and withdrawals for qualifying medical expenses are not taxed.

You may also access funds in your HSA to pay the premiums for most long-term-care insurance policies. The annual withdrawal depends on your age, ranging from $480 per year if you are 40 or younger to $5,960 if you are 71 or older (IRS through 2023).

- That leads us to long-term care insurance (LTCI). LTCI isn’t cheap, and you won’t qualify if you have a pre-existing debilitating condition, but a policy can provide support when you most need it. Many seek coverage in their 50s or 60s, and coverage will vary considerably.

Most policies are triggered when you are unable to perform two or more “activities of daily living” (ADLs) on your own or if you suffer from dementia or a cognitive impairment.

ADLs include bathing independently, using the bathroom without assistance, dressing oneself, getting in and out of bed without help, eating without assistance, and maintaining continence.

However, LTCI has faced significant criticism due to high costs and rising premiums. If you reach a point where you can no longer afford the premium, you risk losing your coverage or having to reduce it, even if you have been paying into the policy for years.

- Louie Valdez of Westlake Village states and as the name suggests, LTCI is insurance. It is something you hope you never need. If it is unused, the cost provides peace of mind but not much else.

Enter the long-term care annuity. How does this work? You pay a lump sum or regular premium that provides a benefit that can be used for long-term care expenses. If the LTCI benefit is not needed, you or your heirs have access.

But this is a complex product. It has benefits and drawbacks. Underwriters may be more willing to accept someone with pre-existing conditions. But you may not have full coverage immediately. Space limitations prevent a deep dive, but it is an option we want you to be aware of.

- Can you self-finance? You can dip into savings to pay for long-term care if you have adequate resources. But it is costly.

According to a Genworth survey, assisted living facility rates increased by 1.4% to an annual national median of $64,200 per year in 2023.

The national annual median cost of a semi-private room in a skilled nursing facility rose to $104,000, an increase of 4.4%, while the cost of a private room in a nursing home increased 4.9% to $116,800.

Further complicating this approach is the indefinite time period that one may require care. If your assets are depleted, Medicaid may become your best option.

- Consider a Roth IRA. There are many benefits to a Roth IRA when compared to a traditional IRA. For example, a Roth is not subject to required minimum distributions. If possible, you may decide to keep funds in your Roth until needed for long-term care or LTCI premiums.

You must be 59 ½ and have held the Roth for at least five years to avoid taxes or penalties. There are no restrictions on how you can use the funds withdrawn from a Roth IRA. This could be one of the most overlooked planning strategies by individuals as noted by Louie Valdez of Westlake Village, CA.

- Using your home equity. A reverse mortgage allows you to access the equity in your home. You do not make monthly payments, but you will receive monthly installments from the lender. The loan is repaid when the borrower no longer lives in the house. Interest and fees are added to the loan balance each month.

If one spouse passes away, the other may stay in the home. A homeowner cannot be pushed out of their home. The payments will not affect your Medicare benefits or Social Security.

- You may also tap equity by taking out a home equity line of credit (HELOC). Unlike a reverse mortgage, there is no requirement to maintain your home, but if you cannot make payments, you risk losing your home.

Concluding thoughts

How you might approach long-term care will depend on your circumstances. We have offered a basic outline of various options. We encourage you to contact us if you have additional questions or concerns. If you have questions regarding taxes, please talk to your tax professional.

Two years and running

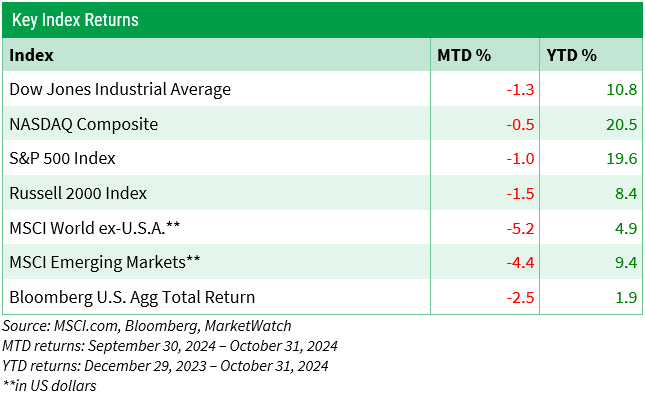

Last month, the bull market turned two years old. Since bottoming on October 12, 2022, the S&P 500 Index has advanced 60% through the last day of October, according to S&P 500 data from the St. Louis Federal Reserve.

The S&P 500 Index is a market-capitalization-weighted index. Simply put, the larger companies in the index have a greater influence than the smaller ones.

Why is this important? On average, the larger companies have outperformed the smaller ones. According to S&P Global, the top ten largest firms in the S&P 500 have nearly doubled since the S&P 500’s Oct 2022 low.

If each stock in the S&P 500 were equally weighted, this measure would have risen a solid 37% from its bottom on October 12, 2022, through October 31, 2024.

What accounts for the discrepancy? In part, the AI revolution has helped several large tech firms significantly outperform the broader market.

Let us review one more index. The granddaddy of market averages, the Dow Jones Industrial Average, which is comprised of thirty companies, touched its most recent bottom on September 30, 2022. It is up an impressive 45% through the end of October, per St. Louis Federal Reserve data.

But market strength extends beyond technology. The surprisingly resilient U.S. economy has helped fuel profit growth, which has helped drive equities higher.

While AI and a resilient U.S. economy have been significant factors, let us consider one more. The rate of inflation has slowed, taking pressure off the Federal Reserve, which hiked interest rates sharply in 2022.

The Fed has begun to slowly take its foot off the monetary brakes, with a much-anticipated rate cut near the end of September. It was the first reduction in interest rates by the Fed since early 2020.

Most investors believe the Fed will reduce interest rates through the remainder of the year, once in November and once in December.

But the pace next year turns murky.

Will the inflation rate continue to slow and gradually return to the Fed’s target of 2%? Will Fed policy help guide the economy to what is called an economic soft landing? A soft landing is loosely defined as a slowdown in economic growth that leads to lower inflation without a recession.

Or will economic growth remain strong, boosting corporate profits while slowing or ending rate cuts?

Or – let us consider one more scenario—will the economy fall into a recession?

Economic forecasters have traditionally struggled to pinpoint the onset of a profit-killing recession. Recessions tend to sneak up on economists. That said, you may recall in 2022, recession forecasts were widespread. Nonetheless, many of the brightest economic minds fell flat with their predictions.

Given today’s bull market, paraphrasing what we said last month bears repeating.

Robust market performance sometimes leads to euphoria that can encourage too much risk-taking. We caution against that.

Leaning heavily into stocks may underpin returns, but unexpected volatility from any number of sources can spark shorter-term declines that extend beyond one’s comfort level.

A balanced approach based on your individual financial goals and tolerance for risk helps tap into the long-term potential stocks have historically offered while helping to diminish some of the downside risks that can materialize when markets unexpectedly decline.

I trust you have found this review to be informative. If you have any questions or wish to discuss other matters, please do not hesitate to contact me or any team member.

As always, thank you for choosing us as your financial advisor. We are honored and humbled by your trust.

Louie Valdez of Westlake Village, CA is a former financial advisor with major Wall Street firms.